Under Pressure: The Top 3 Challenges Facing Health Insurance Brokers, PEOs, and Health Plans in 2026

YL

The organizations that touch employer-sponsored and government health coverage in the Southeast — insurance brokers, professional employer organizations (PEOs), and health plans — are all wrestling with a version of the same storm: healthcare costs are climbing faster than in more than a decade, margins are thinning, and technology is rewriting the rules of who wins. But each type of organization feels that storm differently. Understanding exactly where the pressure lands, and what it costs them, is the first step to figuring out how partners and solution providers can actually help.

Below is a look at the three biggest challenges facing each of these three critical organizations right now, and the real business impact each one is having.

Part 1: Health Insurance Brokers

Challenge 1: Commission compression and shifting compensation models

For decades, brokers built their businesses on a predictable commission structure. That foundation is cracking. Smaller generalist agencies — those under roughly $5 million in revenue — are getting squeezed hardest, facing both commission compression and rising operational demands at the same time. Nowhere has this been more dramatic than in Medicare Advantage. Heading into 2026, some carriers cut or even eliminated broker commissions on more than 100 plans across 20-plus states, in some cases making mid-year changes after contracts had already been finalized — a move brokers publicly called a "bait-and-switch." Regulators have grown so concerned that carriers are using commission cuts to quietly steer beneficiaries away from costly plans that CMS stepped in to adjust agent compensation.

The impact: Revenue predictability — the thing that made brokerages attractive, financeable businesses — is eroding. Brokers are being forced to diversify into fee-based advisory models, add risk-management consulting, and chase industry specializations (healthcare, construction, manufacturing) where commissions still command a 2-to-4 point premium. Those that can't adapt are becoming acquisition targets rather than independent operators.

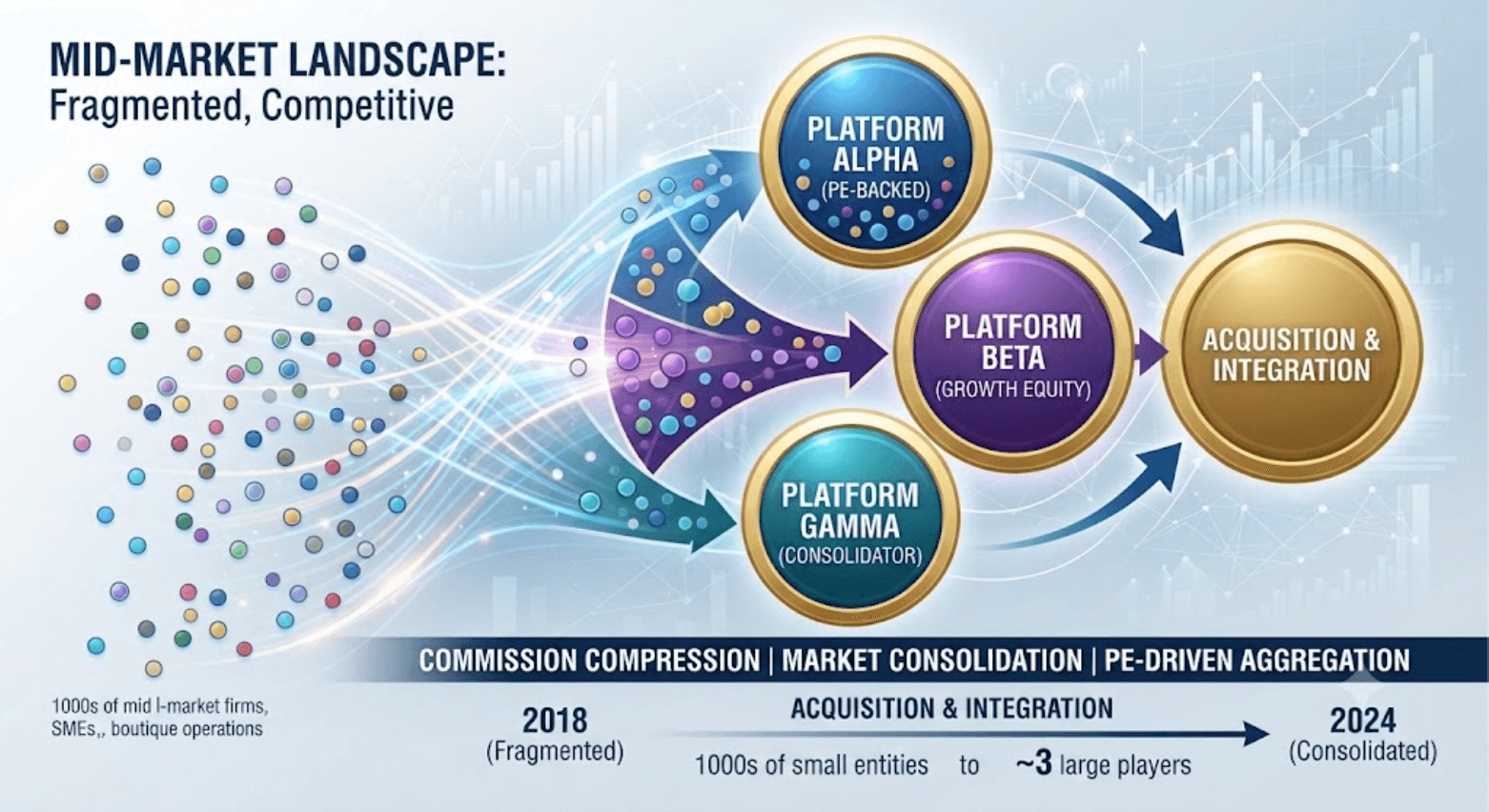

Challenge 2: Relentless consolidation

The brokerage landscape is consolidating at a breakneck pace, and it is reshaping competitive dynamics across the Southeast. Transaction volume rose 17% over a recent twelve-month stretch, and the deals keep getting bigger: Baldwin acquired Cobbs Allen for $1.41 billion, Brown & Brown absorbed the parent of Risk Strategies and One80 for $9.8 billion, and Gallagher swallowed Orlando-based AssuredPartners for $13.45 billion. Private-equity-backed platforms now command valuation multiples up to 2.7 times higher than traditional agencies, and top-quartile players use their scale to negotiate commission enhancements averaging 12% above standard schedules.

The impact: Independent and mid-market brokerages face a widening scale disadvantage. The large aggregators win on carrier access, pricing leverage, and technology investment — advantages a local shop simply can't match. Consolidation also creates hidden operational drag: merged firms often run incompatible agency management systems, producing data bottlenecks and painful, time-consuming integrations that distract from client service. For many independent brokers, the strategic question is no longer "how do I grow?" but "do I sell, or do I find a defensible niche the big players can't be bothered to fight for?"

Challenge 3: Rising client costs and the pressure to prove value

A broker's core promise is to protect clients from cost increases — and that promise is getting harder to keep. The average annual premium for employer-sponsored family coverage reached $26,993 in 2025, up 6%, and employers expect health-benefit costs to jump about 6.5% per employee in 2026, the largest increase in more than a decade. Some projections put the total cost of health benefits up as much as 9%. When clients open renewal packets and see double-digit increases, the broker is the one in the room who has to explain it.

The impact: Brokers are being pushed to evolve from transactional plan-placers into strategic cost-containment advisors. Those who can proactively bring cost-saving strategies — alternative funding, wellness and utilization management, data-driven plan design — become indispensable. Those who simply "shop the market" once a year look increasingly replaceable, especially as AI-enabled platforms threaten to deliver that commoditized function at a structurally lower cost.

Part 2: Professional Employer Organizations (PEOs)

Challenge 1: Rising healthcare costs inside the master plan

The PEO value proposition is built on pooled purchasing power — aggregating thousands of small employers into master health plans that secure Fortune-500-level rates. But the same medical inflation hammering everyone else is now testing that model. Milliman's 2026 Medical Index estimated employer-sponsored healthcare costs rising 7.9% in 2026, with pharmacy and outpatient facility spending accounting for 69% of the increase. Small-group premiums specifically could climb 9-11%. When the pooled plan's costs rise, the PEO must either absorb the hit or pass it along — and passing it along undercuts the very affordability that attracts clients.

The impact: Healthcare cost trend has become the central strategic challenge of the PEO industry — what some in the sector call "the PEO paradox": the rising costs that make PEOs attractive to small employers also threaten the economics of the pooled plans they depend on. PEOs that can bend the cost curve through chronic-disease management, wellness programs, utilization review, and smarter plan design turn a threat into a competitive advantage. Those that can't watch their core differentiator erode.

Challenge 2: Intensifying competition and the demand for more than admin

PEOs are no longer competing only with each other. Payroll giants, HR-tech platforms, and venture-backed newcomers are all crowding into the co-employment and HR-outsourcing space, and clients now expect far more than payroll and compliance. Value-added services — talent acquisition support, learning platforms, HR technology, and increasingly healthcare navigation and wellness — are projected to be the fastest-growing category in the North American PEO market, expanding nearly 12% annually. The market itself is growing (from roughly $6.86 billion in 2025 toward a projected $10.43 billion by 2031), which only draws more competitors in.

The impact: The sales conversation has moved decisively beyond administrative relief. With 67% of small and mid-sized businesses citing hiring difficulties and 62% citing retention as major challenges, PEOs increasingly win or lose on whether their benefits and wellness offerings actually help clients attract and keep talent. This is pushing PEOs to bolt on new employee-support layers — VensureHR's 2026 launch of a guided healthcare-and-wellness navigation product is a telling example. The upside: as PEOs add these tools, switching costs rise and revenue per client deepens. The risk: PEOs that stay stuck on payroll-and-compliance messaging get commoditized.

Challenge 3: An ever-expanding compliance burden

Compliance complexity is the workload that never stops growing, and it is a double-edged sword for PEOs. On one hand, it's a primary reason employers sign up. On the other, it's a relentless operational cost. Thirteen states plus D.C. have enacted paid family and medical leave programs, with Delaware's taking full effect in January 2026. California layered on new pay-data reporting requirements and strengthened enforcement. Federal wage-and-hour rules, benefit-plan requirements, evolving legislation like OBBBA, new pharmacy-benefit-manager transparency rules, and the IRS Certified PEO framework all demand consistent, error-free execution across every state a client operates in.

The impact: Multi-state and remote workforces have turned compliance into a genuine competitive moat — but only for PEOs with the infrastructure to execute flawlessly. Every new state program is another reporting calendar, tax rule, and eligibility standard that must be tracked perfectly, because a single misstep exposes both the PEO and its clients to penalties. For well-run PEOs, this complexity is a durable reason clients don't leave. For under-resourced ones, it's a mounting liability.

Part 3: Health Plans and Payers

Challenge 1: Medicare Advantage margin compression

For years, Medicare Advantage was the profit engine of the payer world. That engine is sputtering. Margins have shrunk as seniors use more care, medical services get more expensive, and regulatory changes tamp down reimbursement. The response has been stark: UnitedHealthcare, Humana, and Aetna all reduced the number of states and counties they serve for 2026 to protect margins, and an estimated 3 million people were pushed out of soon-to-be-terminated MA plans and forced to find new coverage. The 2027 Advance Notice signals still more compression ahead as risk-adjustment rules tighten.

The impact: Payers are retreating from unprofitable markets, narrowing networks, and shifting more cost onto members — all of which strain member satisfaction at the worst possible moment. The strategic pivot underway is toward care management, member experience, and data analytics: plans are redirecting resources to defend profitability rather than chase enrollment growth at any cost. For Southeast regional plans, the pressure is acute because they lack the geographic diversification of the national carriers to absorb losses in any single market.

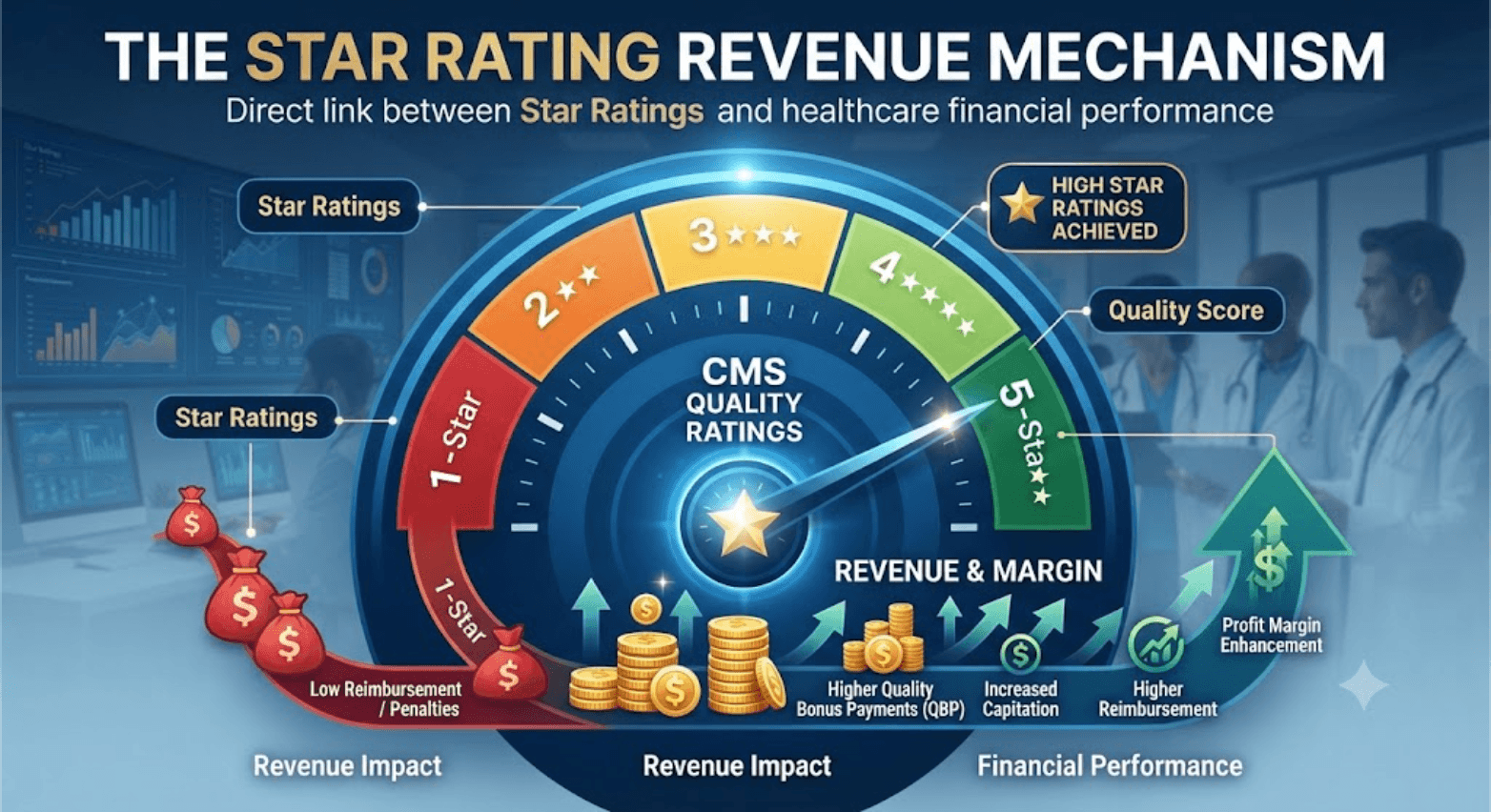

Challenge 2: Star Ratings and the revenue they control

In Medicare Advantage, quality Star Ratings aren't just a report card — they directly dictate revenue through Quality Bonus Payments, and therefore a plan's ability to fund the supplemental benefits that attract members. After years of decline, ratings stabilized for 2026 but showed little real improvement: only about 40% of MA contracts earned four stars or higher, and roughly 64% of enrollees are in 4-plus-star plans. The stakes are enormous. When members shift out of 4-star tiers, plans lose bonus dollars outright — Humana's largest contract remained below four stars, and the company expects most of its members to be in sub-4-star plans in 2026, a multi-billion-dollar problem it's trying to solve through "contract diversification."

The impact: Star performance now directly determines financial flexibility and market positioning. There's a notable Southeast bright spot: GuideWell Health (Florida Blue) shifted nearly 24% of its membership from 3-star to 4-star plans — exactly the kind of move that unlocks bonus revenue and competitive benefit designs. Plans are pouring investment into the measures that drive ratings: care-gap closure, member engagement, patient experience, and outcomes. This is precisely where member-facing wellness, engagement, and remote-monitoring solutions can move the needle — improving the outcome and experience scores that Stars reward.

Challenge 3: Medical loss ratios pressing against the ceiling

Underneath everything sits a squeeze on the fundamental math of insurance. Across commercial and government lines, average medical loss ratios (MLRs) — the share of premium spent on care — have crept toward 88-90% for many regional and mid-size plans, leaving almost nothing for administration, investment, or growth. National health-plan net income declined meaningfully in 2024 as loss ratios climbed and cash flows tightened. MA enrollment growth has outpaced premium adjustments, creating structural mismatches in risk-adjusted revenue.

The impact: When MLRs push against regulatory ceilings, every dollar of administrative waste or avoidable medical spend becomes existential — especially for the regional and provider-sponsored plans common across the Southeast, which don't have national scale to fall back on. The highest-performing plans are responding by building unified data platforms, deploying predictive risk models to intervene before costly acute episodes, and forming performance-based operational partnerships. In other words, the plans that survive MLR pressure are the ones that get proactive about member health rather than reactive to claims.

The Common Thread

Look across all three organizations and a single pattern emerges: rising healthcare costs are compressing everyone's economics, and the winners are the ones who shift from transactional, reactive models to proactive, outcomes-driven ones. Brokers must become strategic cost advisors. PEOs must deliver wellness and talent outcomes, not just payroll. Health plans must improve member health to protect their margins and their Star Ratings.

That shared pivot — from processing to outcomes, from administration to engagement — is exactly where the future opportunity lies. The organizations that help brokers, PEOs, and health plans actually improve the health and engagement of the people they serve won't just be vendors. They'll be the partners that turn each of these three challenges into a competitive advantage.